Vega: The options Greek

Vega is a popular option Greek that measures the sensitivity of an option's price to changes in the implied volatility of the underlying asset. It is a valuable tool for options traders as it provides them with an understanding of the potential impact of changes in volatility on their options positions. In this blog post, we will explore Vega in more detail and discuss how traders can use it to their advantage.

What is Vega?

Vega (ν) also known as kappa or lambda, is one of the options Greeks that measures the change in the price of an option for every 1% change in the implied volatility of the underlying asset. Implied volatility is a measure of the market's expectations of how much the price of the underlying asset will fluctuate in the future. Vega is expressed as a positive number and is usually measured in Indian rupees.

How to calculate Vega?

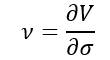

The formula for calculating Vega is:

Where:

- ∂ – the first derivative

- V – the option’s price (theoretical value)

- σ – the volatility of the underlying asset

To calculate the Vega of an option, you need to take the partial derivative of the option price with respect to the implied volatility. This can be done using an options pricing model such as the Black-Scholes model. However, most options trading platforms provide Vega as one of the standard options Greeks, so traders do not need to calculate it themselves.

For example, suppose the Vega of an option is INR 0.50. This means that for every 1% increase in implied volatility, the price of the option will increase by INR 0.50.

How does Vega impact option prices?

Vega is a measure of an option's sensitivity to changes in implied volatility. When implied volatility increases, the option's price will increase, and when implied volatility decreases, the option's price will decrease. This is because an increase in implied volatility increases the probability of the option expiring in the money, which increases its value. Similarly, a decrease in implied volatility decreases the probability of the option expiring in the money, which decreases its value.

Vega is also important because it can affect the rate of time decay of an option. Time decay refers to the reduction in the value of an option as it approaches its expiration date. The higher the Vega of an option, the faster it will decay as volatility decreases. Conversely, the lower the Vega of an option, the slower it will decay as volatility decreases.

How to use Vega in options trading?

Vega is a crucial tool for options traders as it allows them to evaluate the potential impact of changes in volatility on their options positions. By analyzing the Vega of an option, traders can determine how much risk they are taking on and adjust their positions accordingly. Here are some ways that traders can use Vega in their options trading strategies:

- Hedging: Traders can use Vega to hedge their options positions against changes in implied volatility. By buying or selling options with opposite Vega values, traders can create a neutral position that is less affected by changes in volatility.

- Adjusting position size: Traders can use Vega to determine how many options contracts they should buy or sell to achieve their desired level of risk. Options with higher Vega values are more sensitive to changes in implied volatility, so traders may choose to buy fewer contracts to reduce their exposure to volatility.

- Choosing options strategies: Traders can use Vega to select options strategies that are best suited to their risk tolerance and trading style. Strategies that involve buying options with high Vega values, such as long straddles or long strangles, are more sensitive to changes in implied volatility, while strategies that involve selling options with low Vega values, such as short straddles or short strangles, are less sensitive to changes in implied volatility.

Conclusion:

In conclusion, Vega is a critical option Greek that measures the sensitivity of an option's price to changes in the implied volatility of the underlying asset. It is a valuable tool for options traders as it provides them with an understanding of the potential impact of changes in volatility on their options positions. Traders can use Vega to hedge their options positions against changes in implied volatility, adjust their position sizes to achieve their desired level of risk, and select options strategies that are best suited to their risk tolerance and trading style.

It's important to note that Vega is just one of the many options Greeks that traders use to evaluate the potential risk and reward of their options positions. Traders should also consider other options Greeks, such as Delta, Gamma, Theta, and Rho, to get a complete picture of their options positions.

Learn Option series next reads: