Delta: A Deep Dive into the Options Greek

In the world of options trading, it is essential to understand the various metrics that help traders assess the risk and potential reward of a trade. One of the most crucial metrics is delta, which is one of the Greek letters used to denote the sensitivity of an option's price to changes in the underlying asset's price. Delta is a crucial Option Greek because it provides traders with an idea of how an option will react to changes in the underlying asset's price. In this blog, we will explore delta in detail, including what it is, how it is calculated, and how traders can use it to their advantage.

What is Delta?

Delta(Δ) is one of the most important Option Greeks, and it is used to describe the sensitivity of an option's price to changes in the price of the underlying asset. Delta is a measure of the degree to which an option's price will change in response to a one-point movement in the underlying asset's price.

In simple terms, delta tells traders how much an option's price will increase or decrease for every $1 movement in the underlying asset's price. Delta is always expressed as a number between -1 and 1, and it can be either positive or negative, depending on whether the option is a call or put option.

Delta for Call Options

For call options, a delta is always a positive number that ranges between 0 and 1. The delta of a call option tells traders how much the option's price will increase for every $1 increase in the price of the underlying asset.

For example, if the delta of a call option is 0.5, then the option's price will increase by $0.50 for every $1 increase in the underlying asset's price.

The delta of a call option is highest when the option is deep in the money, meaning that the option has a high intrinsic value relative to its strike price. As the option moves out of the money, the delta decreases, meaning that the option's price is less sensitive to changes in the underlying asset's price.

Delta for Put Options

For put options, a delta is always a negative number that ranges between -1 and 0. The delta of a put option tells traders how much the option's price will decrease for every $1 increase in the price of the underlying asset.

For example, if the delta of a put option is -0.5, then the option's price will decrease by $0.50 for every $1 increase in the underlying asset's price.

The delta of a put option is highest when the option is deep in the money, meaning that the option has a high intrinsic value relative to its strike price. As the option moves out of the money, the delta decreases, meaning that the option's price is less sensitive to changes in the underlying asset's price.

Calculating Delta

Delta is calculated using a complex mathematical formula that takes into account a range of variables, including the price of the underlying asset, the strike price of the option, the time until expiration, and the implied volatility of the underlying asset.

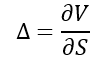

Mathematically, the delta is found by:

Where:

- ∂ – the first derivative

- V – the option’s price (theoretical value)

- S – the underlying asset’s price

However, there are some simple rules of thumb that traders can use to estimate delta. For example, the delta of an at-the-money option is usually around 0.5, meaning that the option's price is roughly half as sensitive to changes in the underlying asset's price as the stock itself. Similarly, the delta of an in-the-money option is usually higher than 0.5, while the delta of an out-of-the-money option is usually lower than 0.5.

Using Delta in Options Trading

Delta is a crucial tool for options traders, as it can be used to assess the risk and potential reward of a trade. Traders can use delta to determine the probability of an option expiring in the money.

For example, if a call option has a delta of 0.7, then there is a 70% probability that the option will expire in the money. Conversely, if a put option has a delta of -0.4, then there is a 40% probability that the option will expire in the money.

Traders can also use delta to create hedging strategies that offset the risk of an options position. For example, if a trader has a long call option position with a delta of 0.5, they can hedge their position by shorting an equivalent amount of the underlying asset. This will create a delta-neutral position, meaning that the trader is not exposed to price movements in the underlying asset.

Another way that traders can use delta is to adjust their options positions as the underlying asset's price changes. For example, if a trader has a long call option position with a delta of 0.7, and the underlying asset's price starts to rise, the delta of the option will also increase. The trader can then adjust their position by selling some of the underlying assets or buying more call options to maintain a delta-neutral position.

Conclusion

Delta is one of the most important option Greeks, as it provides traders with an idea of how an option will react to changes in the underlying asset's price. Delta is a measure of the degree to which an option's price will change in response to a one-point movement in the underlying asset's price. Delta is always expressed as a number between -1 and 1, and it can be either positive or negative, depending on whether the option is a call or put option. Traders can use delta to assess the risk and potential reward of trade, create hedging strategies, and adjust their options positions as the underlying asset's price changes. Overall, understanding delta is essential for anyone interested in trading options.

Furthermore, it is important to note that theta is not the only Greek that investors should consider. Theta, gamma, rho, and vega are also important measures that investors and traders need to understand.

Learn Option series next reads: