Is this the Calm before the Storm?

Discover how markets have reacted to past Fed rate cuts and explore how different asset classes fared during recessionary times

As the world watches, the Federal Reserve stands at the center of attention, poised to make decisions that ripple through the economy. The notion of a Fed rate cut has become more than just a headline—it’s a signal that something deeper is unfolding in the financial world. For some, it’s a beacon of relief, a chance for economic momentum to build again. For others, it's a sign of storm clouds on the horizon. But what exactly is a Fed rate cut, and why does it stir up so many emotions across markets and beyond?

Dive into this blog to uncover:

Uncover the Signals of a Recession: What key indicators suggest that the U.S. may already be in a recession? Dive into our analysis of the yield curve, GDP growth, and inflation trends to understand the economic signals you can't afford to ignore.

The Performance of Asset Classes: How do different asset classes respond during economic downturns? Discover the historical performances of equities, gold, and bonds during the 2007-2009 financial crisis and what this means for your investment strategy today.

Navigating Indian Markets Amidst Global Uncertainty: How do U.S. economic trends influence the Indian market? Explore the correlation between U.S. rate changes and India's market performance, and learn how to adjust your investment strategy accordingly.

Crafting Your Investment Strategy: Are you an aggressive or conservative investor? Uncover tailored strategies for both risk-takers and cautious investors, and find out how to position your portfolio for stability and growth in uncertain times.

At its core, a Fed rate cut is a reduction in the federal funds rate—the interest rate at which banks lend to one another overnight. This rate, though seemingly small, is like the heartbeat of the economy, controlling the flow of money and the cost of borrowing for consumers and businesses alike. When the Fed cuts rates, it’s a move to stimulate a slowing economy, making borrowing cheaper and nudging people and companies to spend and invest more.

But why is the Fed considering such a move now? The answer lies in the current economic landscape. Inflation, once running hot, has begun to ease, but growth has also cooled. The job market, once resilient, is showing signs of strain, and investors are beginning to ask the hard questions: Has the Fed waited too long to act? Or is this rate cut a necessary step to keep the economy from tipping into a full-blown recession?

The fear of recession looms large. Some look at rising unemployment and slowing job creation, while others point to shaky consumer confidence and cooling spending. Still, despite these uncertainties, there’s a divide. Some believe that this is merely a slowdown, a temporary pause in growth. Others fear it’s the beginning of something more severe—a recession that could reshape the global economy.

For many, these fears are heightened by memories of the 2008 financial crisis. Back then, a similar combination of factors—collapsing housing markets, distressed financial institutions, and rapid rate cuts—triggered one of the deepest recessions in modern history. Investors and economists are now watching for parallels, questioning whether this time will mirror 2008. How will assets like stocks, bonds, real estate, and commodities react? During the 2008 crisis, stock markets plunged, bonds became a safe haven, and real estate faced a prolonged slump. The question today is whether we’ll see the same pattern or if new dynamics will drive different outcomes this time around.

As we dive deeper into the topic, this magazine will explore these questions, looking at why the Fed cuts rates, the signals of an economic downturn, and how these actions reverberate across different asset classes, from stock markets to global trade. We’ll also consider the fears driving concerns about a looming recession and how these economic moves impact the U.S., India, and the rest of the world. Most importantly, we’ll examine whether this potential recession will follow the script of 2008—or chart a different course entirely.

So, buckle in. The journey through the twists and turns of rate cuts, market reactions, and economic shifts is just beginning.

Riding the Waves of Economic Change: The Fed’s Rate Cut Journey

History doesn’t exactly repeat itself, but when it comes to the Federal Reserve’s interest rate decisions, it certainly rhymes. Every rate cut is a pivot that sends ripples through stock markets, currencies, and the lives of people around the world. As we look ahead to another potential Fed rate cut this September, it’s important to step back and examine the rich history behind these decisions.

This is not just a walk through the past—it's a deep dive into how the Fed has shaped the economy for decades, helping us understand the path we’re on today. From bold decisions in times of crisis to carefully measured moves during times of stability, each rate cut reveals a story of economic resilience, reaction, and renewal.

The Volcker Shock: Beating the Great Inflation (1981-1990)

In the early 1980s, the U.S. economy was under siege by soaring inflation. At its worst in 1980, inflation hit a shocking 14.6%. Paul Volcker, the Federal Reserve Chair, was determined to rein it in, even if it meant short-term pain. He hiked interest rates to an unprecedented 20%—levels unimaginable today. This aggressive move, known as the "Volcker Shock," triggered a recession, but it worked. By 1986, inflation had dipped below 2%.

Volcker’s harsh methods were controversial at the time—protestors gathered outside the Fed’s doors—but the long-term effects were undeniable. The lessons? Sometimes, an economy needs tough love. Volcker’s moves laid the groundwork for decades of economic stability and cemented the importance of decisive central banking during crises.

The Greenspan Era: Stability Amid Bubbles (1991-2000)

The 1990s brought a shift in economic philosophy. Under Alan Greenspan, the Fed moved to preemptive rate cuts, not in response to a crisis, but to prevent one. After a short recession in 1990, Greenspan’s Fed cut rates in 1995 and 1998, shielding the U.S. from global shocks like Russia’s debt default and the collapse of Long-Term Capital Management.

This was a period of steady growth and low inflation, a time many called the “Great Moderation.” However, low rates helped fuel the dot-com bubble, a risky surge in tech investments that burst spectacularly at the turn of the century. The moral? Preemptive cuts can stave off downturns but may also sow the seeds of future instability.

The Dot-Com Bust and 9/11: Surviving Twin Shocks (2001-2003)

The dawn of the new millennium saw the collapse of the dot-com bubble, wiping out billions in tech investments. The Nasdaq plunged by 78%, dragging the economy into recession. In response, the Fed slashed interest rates 13 times from 2001 to 2003, dropping them to a then-unheard-of 1%.

This period also saw the 9/11 attacks, leading to further emergency cuts to calm markets. While these measures helped stabilize the economy, they also set the stage for another crisis—the housing bubble. It was a reminder that while rate cuts can pull economies back from the brink, they sometimes create unintended consequences down the road.

The Great Recession: The Housing Market Crash (2007-2009)

Few economic crises have had the devastating impact of the 2008 financial meltdown. The housing bubble burst, leading to a global financial crisis that brought banks to the edge of collapse and wiped out trillions in wealth. The Fed, under Ben Bernanke, slashed rates to near zero and introduced quantitative easing (QE)—a radical policy of buying bonds to inject liquidity into the economy.

The move was unprecedented but necessary. While the Fed's quick response helped avoid a complete collapse, the scars of the Great Recession remain. The crisis fundamentally reshaped the way central banks approach future downturns, introducing a new era of monetary policy tools that would prove vital in the years to come.

The Covid-19 Pandemic: A New Kind of Crisis (2020)

Just as the world was recovering from the Great Recession, a new and unforeseen crisis struck: the Covid-19 pandemic. The global economy came to a standstill, with GDP contracting sharply and unemployment soaring. The Fed acted swiftly, cutting rates back to zero and re-launching quantitative easing to stabilize markets.

This was the fastest rate-cut cycle in history, with two unscheduled meetings in March 2020 alone. But as the world began to recover, a new challenge emerged: inflation. The unprecedented economic stimulus from 2020 would later fuel the inflation surge of 2021-2022, proving once again that each economic crisis comes with its own unique set of trade-offs.

The Inflation Comeback: Battling High Prices (2022 and Beyond)

By 2022, inflation had returned to levels unseen since the Volcker era, hitting a 40-year high of 9.1%. The Fed, led by Jerome Powell, raised rates rapidly in an effort to combat inflation, increasing them 11 times in just over a year, bringing the federal funds rate to 5.25-5.5%.

Powell’s rate hikes marked one of the fastest tightening cycles in history. The key challenge for the Fed today is finding the right balance—curbing inflation without triggering a recession. It's a familiar dance: walk the line too aggressively, and risk stalling the economy; not aggressively enough, and inflation could spiral further out of control.

Learning from the Past, Preparing for the Future

Looking back at the Fed’s rate cuts over the years reveals a pattern: every cut is a reaction to a unique set of economic circumstances, but each decision also comes with long-term consequences. The Volcker era taught us that sometimes painful decisions are needed to break inflation. The Greenspan and dot-com years showed the dangers of complacency. The Great Recession and Covid crises demonstrated the power—and risks—of extreme monetary policy measures.

As we sit on the edge of another potential rate cut, the lessons of the past are more relevant than ever. While history may not provide a perfect roadmap, it offers a guide—one that reminds us that economic recovery is often a winding path, full of risks, rewards, and the occasional unexpected turn.

The Road Ahead: U.S. Economic Forecast for 2024 and Beyond

As we step further into 2024, the U.S. economy continues to surprise analysts with its resilience. Despite ongoing challenges, elevated interest rates, and a rapidly evolving global landscape, the forecast remains optimistic — for now. Inflation is gradually easing, and no major economic crisis looms on the horizon. Economists are cautiously optimistic that a full-blown recession might be averted. But with the road ahead still uncertain, what are we really expecting over the next year, and how might the Federal Reserve’s next moves shape the outcome?

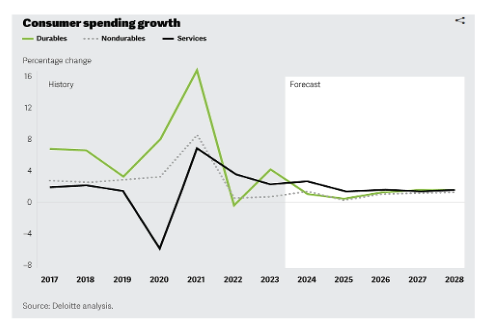

While the U.S. economy grew steadily at 2.5% in 2023, fueled by solid consumer spending and business investment, 2024 has already shown signs of slowing down. Job growth, which had remained strong, has started to cool. According to Deloitte’s baseline scenario, real GDP growth is expected to land around 2.4% this year, with a further deceleration to 1.7% in 2025. While these numbers indicate continued growth, they also reveal a slower pace, signaling that the economy is facing some challenges ahead.

Economists agree that global uncertainties, including geopolitical tensions, inflationary pressures, and trade disruptions, remain risks. If issues such as higher oil prices or rising tariffs reassert themselves, the Fed might need to adopt a tighter monetary stance than currently anticipated. In a more pessimistic scenario, this could result in GDP growth dipping as low as 0.6% by 2025. However, for now, forecasts remain balanced between growth and potential risk factors.

According to market experts and economists, the equity markets are not anticipating continuous sharp rate cuts. However, should the Fed implement more aggressive rate cuts, a market correction could occur. Nonetheless, the impact may not be severe, as a 2-3% rate decline has already been priced into market expectations.

Consumers: Resilient, But for How Long?

Consumer spending has been one of the most surprising strengths of the U.S. economy. Despite the pressure of higher interest rates and inflation, American households have maintained a strong rate of spending, dipping into pandemic-era savings and even taking on more debt. But this cannot go on forever. By the second half of 2024, economists predict that consumer spending will begin to taper off as disposable income growth fades. For now, spending is forecasted to grow at 2.2% for 2024, gradually slowing to 1.8% in 2025.

Disinflation in Sight?

After several years of high inflation, it finally appears to be cooling. By mid-2024, core inflation eased to 3.2%, its lowest level since 2021. Economists expect this trend to continue, with the Federal Reserve’s preferred inflation measure, the personal consumption expenditures (PCE) index, forecasted to hit 2.5% by year-end. However, the road to full disinflation won’t be smooth. The economy is still vulnerable to global disruptions, such as supply chain issues and commodity price volatility, which could cause inflation to flare up again.

To combat lingering inflationary pressures while fostering growth, the Fed is expected to gradually cut interest rates. Economists forecast that the Fed will enact three rate cuts by the end of 2024, with further reductions expected through 2025 and 2026. These cuts, economists say, will provide much-needed relief for businesses and consumers alike, without igniting another inflationary spiral.

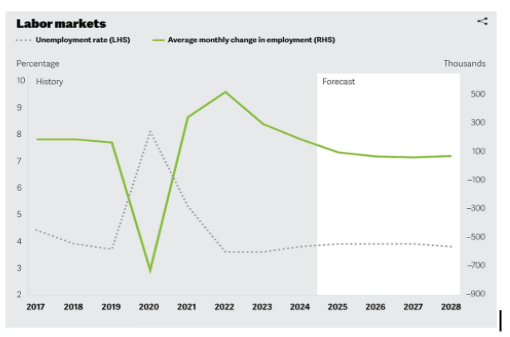

Labor Market: Cooling, But Stable

The U.S. labor market, which remained strong through the first quarter of 2024, is starting to show signs of softening. The unemployment rate has inched up to 4.3%, and wage growth has begun to slow. Despite this, the fundamentals of the labor market remain robust, and economists predict the unemployment rate will stay relatively stable at around 4.4% to 4.5% over the next two years.

A key factor driving this resilience is the changing nature of the U.S. workforce. As the population ages, job growth is expected to slow, presenting new challenges for employers and policymakers alike. However, even modest job gains will take on greater significance, as the labor market adjusts to these demographic changes.

Business Investment and Financial Markets: Navigating Uncertainty

Business investment has been another bright spot, with sectors like manufacturing and technology driving growth. Despite the high cost of borrowing, business investment is expected to grow by 3% in 2024. The Inflation Reduction Act, with its incentives for renewable energy and advanced technologies, has provided a welcome boost to the economy. However, concerns about financial stability remain, especially in the real estate sector.

As the Federal Reserve begins its series of rate cuts, financial markets are expected to adjust. Markets have already priced in a 25 basis point cut in September 2024, with further cuts likely to follow. While these cuts are expected to foster a more favorable environment for investment, uncertainty remains — particularly in light of potential geopolitical disruptions and trade tensions.

The Soft Landing Debate

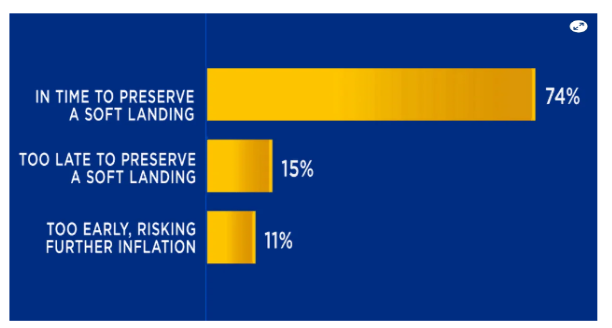

This brings us to the million-dollar question: Will the U.S. achieve a soft landing? Economists are divided on the subject. On one side, those optimistic about the Fed’s gradual approach to rate cuts believe it will be enough to sustain moderate growth without tipping the economy into a recession. In fact, a recent survey by CNBC found that 74% of respondents believe the Fed’s rate cuts will help preserve a soft landing. They argue that inflation is easing, consumer spending is still strong (though slowing), and the economy is growing faster than expected.

Others, however, remain skeptical. Some economists worry that the Fed’s efforts may be too little, too late. They point to the rising unemployment rate, cooling job growth, and fading consumer confidence as signs that the window for achieving a soft landing is narrowing. Some even suggest that the Fed’s reluctance to cut rates more aggressively could result in a more significant economic downturn.

Ultimately, the probability of a soft landing stands at about 53%, with the likelihood of a recession at around 36%. While the road ahead remains uncertain, the U.S. economy’s performance over the next year will largely hinge on how well the Fed navigates its rate cuts and the global risks that could derail the recovery.

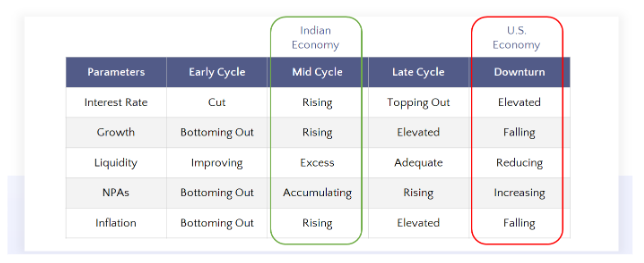

Is the Recession Already Here? Breaking Down the Signals

When analyzing the state of the economy, it's essential to understand where different regions fall within the broader economic cycle. The table we have provides a comprehensive look at both the Indian and U.S. economies in various stages of the economic cycle, shedding light on how far they’ve progressed and what that means for the future.

ECONOMIC CYCLE & CHALLENGES

Let’s first look at the different stages of the cycle:

- Early Cycle: This phase often features interest rate cuts, bottoming out growth, improving liquidity, and rising inflation. Economies in this stage are showing signs of recovery.

- Mid Cycle: As growth rises and inflation becomes more pronounced, economies begin to stabilize. India, for instance, is currently positioned here, with indicators like rising growth and inflation signaling robust economic activity, but also the accumulation of risks such as non-performing assets (NPAs).

- Late Cycle: When economies reach this phase, interest rates start to top out, inflation remains elevated, and liquidity becomes just adequate to maintain operations.

- Downturn: This is where the U.S. economy currently sits, as highlighted in the table. The indicators tell a sobering story: elevated interest rates, falling growth, reducing liquidity, and declining inflation are clear markers of a recessionary environment.

While India remains in the mid-cycle, reflecting growth and stability, the U.S. has entered a downturn. This leads us to the core question: is the recession already here? By looking at specific economic indicators, we can infer that it may already be upon us.

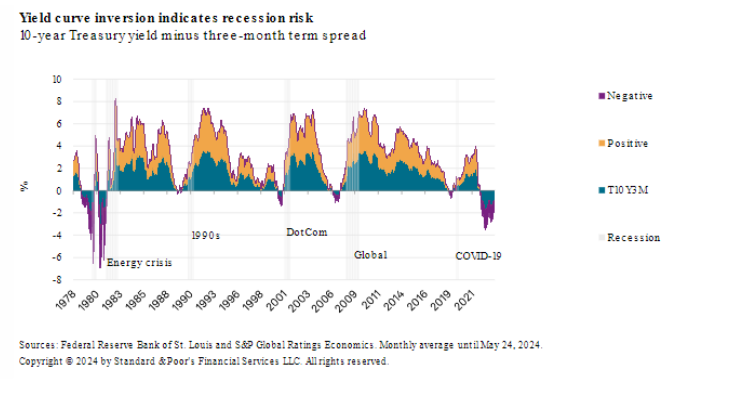

Yield Curve: The Classic Recession Indicator

The yield curve, a crucial indicator of economic health, has long been a predictor of recessions. When the yield curve inverts — meaning long-term interest rates fall below short-term rates — it often signals trouble ahead. Historically, an inverted yield curve has preceded every U.S. recession in recent decades.

At present, the yield curve is inverted, and it’s been this way since 2022. An inverted curve reflects that investors expect future growth to slow significantly, leading to lower long-term interest rates. This inversion typically occurs six to 18 months before a recession officially begins. Given the prolonged inversion, it’s safe to say that the U.S. is already experiencing a significant economic downturn, even if it hasn’t been formally labeled as a recession.

GDP Growth: Signs of Slowing Momentum

Another key indicator to assess whether we’re in a recession is Gross Domestic Product (GDP) growth. In early 2024, U.S. GDP slowed to an annualized rate of 1.3%, down from stronger growth in previous years. On a year-over-year basis, the economy has grown by 2.9%, but economists predict that this figure will soften further as the year progresses.

The U.S. economy is losing momentum, and while it hasn’t yet contracted, the slower growth is characteristic of the downturn phase of the economic cycle. As we head into late 2024, many expect GDP growth to further weaken, potentially dipping below 2%, which is often a hallmark of recessionary conditions.

Inflation: Victory or Ongoing Battle?

Inflation has been a persistent challenge for the U.S. economy. After peaking at 9.1% in June 2022 — a 40-year high — inflation has since moderated. As of August 2024, inflation stood at 2.5%, which may seem like a victory. However, the Fed’s preferred inflation gauge, the core personal consumption expenditures (PCE) price index, suggests otherwise. Core PCE, which strips out volatile food and energy prices, is still running above the Fed’s target at 2.6% year-over-year.

Inflation may be lower than it was at its peak, but the current level is still too high for comfort, especially given the broader economic slowdown. Persistent inflation, coupled with slowing GDP and an inverted yield curve, paints a picture of an economy that’s struggling to regain its footing — classic signals that the U.S. is already in a recessionary phase, or at least on the edge of one.

Conclusion: Reading Between the Lines of the Economic Cycle

When examining the economic cycle and its key indicators, it becomes clear that the U.S. is not waiting for a recession to arrive — it’s likely already here. The inverted yield curve, sluggish GDP growth, and persistent inflation are all signs that the U.S. economy has entered the downturn phase of the economic cycle. While the official label of “recession” may not have been applied yet, the economic signals tell a different story.

As we move further into 2024, it’s important for businesses and investors to recognize that the economy is already in a challenging period and plan accordingly. Whether the recession deepens or stabilizes will depend largely on the Federal Reserve’s next moves, the behavior of inflation, and broader global economic forces.

Capital Preservation or Growth? Choosing the Right Asset Class in Tough Times

As fears of recession loom large in 2024, it becomes essential to revisit historical periods of economic turmoil, such as the 2007-2009 financial crisis, to understand how various asset classes perform during these times. By examining the U.S. and Indian markets during the last significant recession, investors can better prepare for what lies ahead, recognizing which assets thrive and which falter in times of economic uncertainty. Categorizing these assets based on risk will allow investors to make informed decisions, tailoring their portfolios to either weather the storm or capitalize on the high-reward, high-risk nature of downturns.

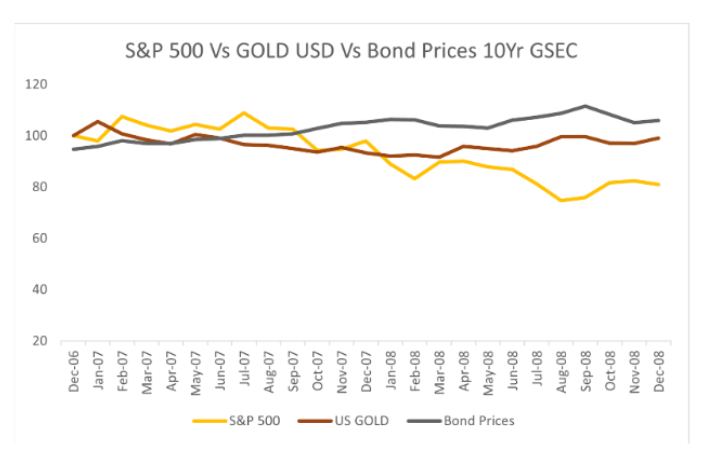

From Stability to Crisis: How Fed Rates and Bond Yields Signaled Recession

Before diving into the facts, it’s important to understand that interest rates and bond yields generally move in the same direction. When the Federal Reserve raises interest rates, bond yields typically increase as borrowing costs rise. On the other hand, when the Fed cuts interest rates, bond yields tend to decline, signaling market expectations of slower economic growth.

From late 2006 to early 2007(Pre-Recession Period), the Federal Reserve's interest rates and the 10-year bond yield remained stable, with a slight upward trend in rates as the Fed tightened policy to address inflation concerns amid a growing economy. However, by mid-2007(Early Signs of Market Stress), a divergence emerged as bond yields declined, signaling investor concerns about future economic growth and a potential slowdown, while the Fed maintained high rates to combat inflation.

As the financial crisis deepened in late 2007 and into 2008, the Fed aggressively cut interest rates in response to the subprime mortgage collapse. Bond yields continued to fall, albeit more slowly than the rapid Fed rate cuts. By the end of 2008, both rates and yields had dropped significantly, with the Fed slashing rates to near-zero to stabilize the economy.

Current Trends: What’s Going On with Fed Rates and Bond Yields?

Currently, bond yields are showing strength, trading at 3.64%, down 30% from 4.70% in May. This decline has occurred despite the Federal Reserve not implementing any rate cuts. This suggests that the market is already pricing in a potential 1-2% rate cut. As a result, we may not see significant volatility in either direction, as the prospect of a rate cut has already been priced.

What’s Driving U.S. Assets? A Look at Equities, Gold, and 10-Year Treasuries

Impact of Fed Interest Rate on the S&P 500 (Equity)

The S&P 500 experienced a significant decline from mid-2007 to 2008 despite the Federal Reserve's aggressive interest rate cuts. Typically, lower interest rates reduce borrowing costs, stimulate economic activity, and support stock markets. However, during the 2007-2008 financial crisis, these cuts couldn't prevent the sharp downturn in equities as the market was gripped by panic, financial institution failures, and looming recession fears. The crisis negated the expected positive effects of lower rates, leading to a prolonged drop in stock prices despite the Fed's interventions.

Impact of Fed Interest Rate on Gold

Gold showed a contrasting response during the same period of interest rate cuts. As the Fed began reducing rates in early 2008, gold prices rose, reinforcing its status as a safe-haven asset. Lower rates make holding non-yielding assets like gold more attractive, especially during economic uncertainty. Investors flocked to gold as a hedge against market instability, pushing prices higher in response to declining stock markets and rising concerns about broader economic conditions.

Impact of Fed Interest Rate on Bond Prices

As the Federal Reserve cut interest rates, yields on 10-year bonds dropped, causing bond prices to rise. This inverse relationship between bond yields and prices made bonds increasingly attractive to investors seeking safety amid the financial crisis. With the stock market in decline and recession fears growing, the demand for bonds surged, resulting in higher prices. The bond market played its traditional role as a refuge for investors during times of economic uncertainty.

Stability vs. Volatility: Analyzing Indian Equities, Gold, and Bonds During Economic Uncertainty

The performance of the Indian economy is often influenced by trends in the U.S. economy, particularly regarding the Federal Reserve's interest rate decisions. As we analyze how various Indian asset classes respond to early signs of recession and actual recession periods, it becomes clear that rational investors prioritize Safety over Returns during these challenging times. While bull markets may present abundant opportunities for investment, both domestically and internationally—such as U.S. bonds and stocks or thematic funds in India—recessionary periods necessitate a shift in strategy. In such times, protecting capital takes precedence over seeking high returns, leading many investors to favor their Home Country for Safety. Consequently, we must examine the historical performance of Indian asset classes during recessions to guide investment decisions in these uncertain economic climates.

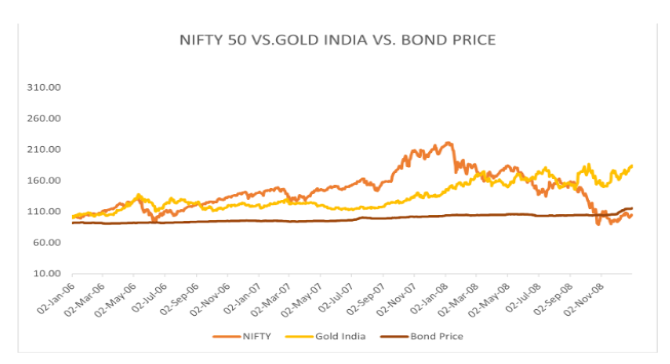

What’s Driving Indian Assets? A Look at Equities, Gold, and Bond

The Fed’s interest rate decisions from 2006 to 2008 played a significant role in shaping global markets, including Indian equities, gold, and bonds. In 2006-2007, as the Fed raised rates to combat inflation, NIFTY 50 rose steadily, fueled by strong economic growth and foreign inflows despite tightening global liquidity. However, when the Fed began cutting rates in late 2007 to address the financial crisis, NIFTY initially rallied but later crashed sharply in 2008, reflecting the impact of global risk aversion and the economic downturn.

Gold, on the other hand, remained stable during the Fed's rate hikes, as rising rates reduced the appeal of non-yielding assets. However, with the onset of rate cuts in 2007-2008, gold surged as investors sought safe-haven assets amid growing economic uncertainty. Lower interest rates reduced the opportunity cost of holding gold, driving its strong performance while stock markets plummeted.

Bond prices were relatively flat throughout this period. Rising rates initially kept bond prices low, but even with rate cuts in 2008, bonds did not experience a significant rally. This was likely due to the broader financial crisis, which led to caution in debt markets, despite the typically inverse relationship between bond prices and interest rates.

As we observe the performance of Equity, Gold, and Bonds, it’s evident that Equity tends to be more volatile during challenging times, while Gold and Bonds offer more stability. In such uncertain periods, investors need to assess their risk tolerance carefully. Safe investors should lean towards Gold and Bonds for protection and consistent returns, while aggressive investors can seek higher potential rewards in Equities, despite the added risk of market swings. Each asset class plays a unique role in navigating market turbulence based on individual risk appetite.

Are You an Aggressive or Safe Investor? Choosing the Right Assets in Tough Times

(Absolute return(%)

(The Crisis Transition Period (2006-08) returns have been calculated in CAGR terms to provide a clearer measure of annualized growth during this volatile phase)

🚀 Ride the Highs, Brave the Lows!

For Aggressive Investors:

- Equities & Gold

- Maximize your growth potential even in uncertain times!

🛡️ Your Shield in Volatile Times!

For Safe Investors:

- Bonds

- Stay secure with steady returns during market swings.