Why Debt Fund may work better for you than FDs?

If you're looking to invest your money in a safe and secure option, you might be considering fixed deposits (FDs) as a traditional investment option. The rate hikes by the RBI have pushed up the lending and deposit rates of banks. Major banks are offering up to 7.5% on fixed deposits of 1-5 years. Before investing in fixed deposits, remember that the interest earned on bank deposits is taxed at normal slab rates. In the 30% tax bracket, the 7.5% interest earned on the fixed deposit on fixed deposit is reduced to just a little over 5% after tax.

One alternative option you might consider is investing in a debt fund. A debt fund is a type of mutual fund that invests in fixed-income securities such as government bonds, corporate bonds, and money market instruments. Here are a few reasons why a debt fund may work better for you than FDs:

- Higher Returns: Debt funds typically offer higher returns than FDs. This is because they invest in a variety of fixed-income securities, which offer different rates of interest. By investing in a diversified portfolio of fixed-income securities, debt funds can offer higher returns than FDs, especially in a low-interest-rate environment.

- Flexibility: Unlike FDs, debt funds offer greater flexibility in terms of investment duration. With an FD, you must lock in your investment for a fixed period, which can range from a few months to several years. However, debt funds allow you to choose your investment duration, which can range from a few days to several years. This means you can choose a debt fund that aligns with your investment goals and needs.

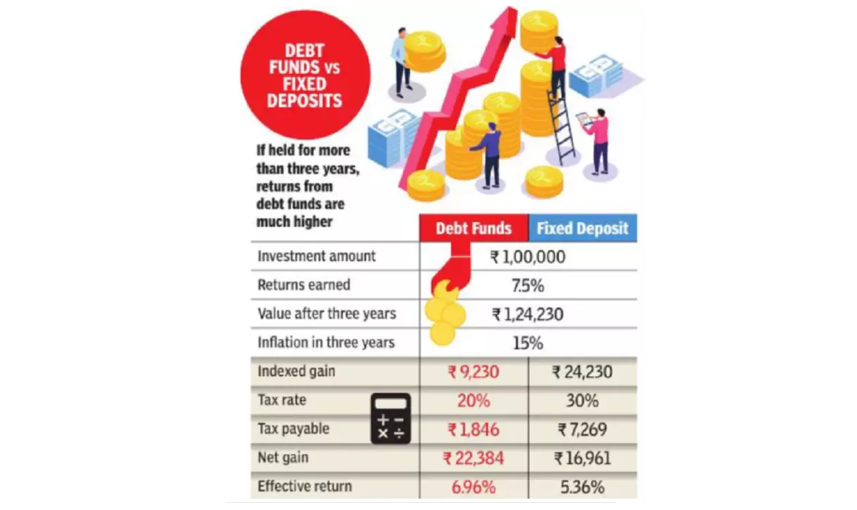

- Tax Efficiency: Debt funds are more tax-efficient than FDs. In India, interest income from FDs is taxed at your slab rate, which means you pay tax on the interest income earned at the same rate as your income tax rate. However, debt funds are subject to capital gains tax, which is more tax-efficient than interest income tax. If you hold your debt fund investment for more than three years, your capital gains are taxed at 20% after adjusting for inflation.

- Liquidity: Debt funds are more liquid than FDs. This means that you can redeem your investment in a debt fund at any time, and the money will be credited to your bank account within a few days. On the other hand, FDs are not very liquid, and if you need to break an FD before its maturity date, you will be penalized.

- Setting Off Gains Against Losses: The gains from these funds can be set off against short term and long-term capital losses on other investments. So, if you made losses in stocks or gold, you can adjust them against the gains from debt funds.

- No TDS On Redemption: There is also no TDS in debt funds. In fixed deposits, if the interest income exceeds Rs 40,000 the bank deducts 10% TDS. A taxpayer who is not liable to pay tax will have to submit either Form 15H or 15G to escape TDS.

If your investment horizon is more than three years, debt funds are a better alternative.

If debt funds are held for more than three years, the gains are classified as long-term capital gains and taxed at 20% after indexation. Indexation takes into account consumer inflation during the holding period and accordingly raises the purchase price of the asset to adjust for inflation. As a result, the effective tax rate for mutual fund investments is much lower than the outgo on fixed deposits.

In conclusion, debt funds offer several advantages over FDs. They offer higher returns, greater flexibility, tax efficiency, and liquidity. However, it's important to remember that debt funds are not risk-free, and you should consult a financial advisor before investing.